SBAB Interim Report Jan-Mar 2025

SBAB’s Interim Report January-March 2025 is now available for download on www.sbab.se/IR.

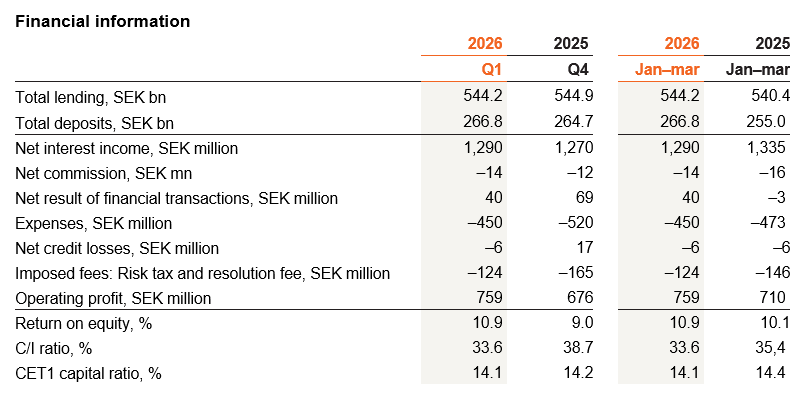

Q1 2025 (Q4 2024)

- Total lending increased 0.5% to SEK 540.4 billion (537.8) concurrent with total deposits decreasing 0.3% to SEK 255.0 billion (255.9).

- Operating profit decreased to SEK 710 million (731), primarily due to a lower outcome for the net result of financial transactions. This trend was somewhat offset by lower costs.

- Net interest income posted a marginal decline to SEK 1,335 million (1,339), mainly due to a quarter-on-quarter increase in expenses linked to the national deposit guarantee. The underlying net interest rate trend was positive.

- Net credit losses totalled SEK 6 million (recoveries: 5). Confirmed credit losses totalled SEK 7 million (4).

- The return on equity amounted to 10.1% (10.1) and the C/I ratio was 35.4% (38.5).

- The Common Equity Tier 1 capital ratio increased to 14.4% (12.7) as a result of the introduction of the Banking Package.

CEO statement from Mikael Inglander:

We continue increasing our market share in mortgages despite intense competition. Our strong growth in deposits has been highly significant for our overall earnings trend in recent years, not least given the pressure on mortgage margins. In early 2025, deposits experienced a trend break, mainly driven by increased outflows of fixed-term retail deposits, which reversed in the latter part of the quarter. The recent global turbulence stemming from the US administration’s announcement of raised tariffs has triggered substantial movements in financial markets and increased uncertainty about future economic developments. SBAB has a strong position with good preparedness and capacity to manage further disruption.

Tariffs cause turbulence and increased uncertainty

The tariffs announced by the USA on imports from countries around the world not only raise international tension, they also increase uncertainty about future economic developments and lead to higher volatility in financial markets. The response to the tariffs by the EU and the rest of the world, and whether these tariffs will be permanent, will be critical for the future development of the economy, inflation and ultimately interest rates. Inflation in Sweden, which surprised on the upside in both January and February, was below expectations in March. The Riksbank’s most recent monetary policy meeting in March decided to leave the policy rate unchanged at 2.25% and concurrently announced that the rate is expected to remain at this level for the entire forecast period. In line with our strategy of acting flexibly to changes in market interest rates, SBAB has continuously adjusted residential mortgage rates. Given the uncertainty in the macroeconomic environment at the time of writing, the interest rate trend is highly uncertain looking forward.

Good growth for mortgages despite challenges

Our total lending volume grew 0.5% in the quarter to SEK 540.4 billion. Growth was particularly strong in mortgages and it is gratifying that, despite fierce mortgage market competition, we continue to grow and capture market shares. This clearly signals our customers’ appreciation of our simple and transparent offer with good terms and conditions. I would also like to showcase our brand and communication initiatives, which have helped us consolidate our position as one of the best-known players in the residential mortgage market. While the trend for the housing market has improved, recent events have generated uncertainty about future developments. The growth rate for residential mortgages increased from 1.4% in December 2024 to 1.7% in February 2025, which is still low from a historical perspective.

Total lending to corporates and tenant-owners’ associations decreased marginally in the quarter. The property sector continues to recover gradually, albeit from low levels, with transaction volumes up and market sentiment slightly more positive. Nonetheless, activity in the new construction market remains very low. The market for lending to tenant-owners’ associations is characterised by a low level of risk, which, in combination with increased loan repayments in a weakly growing market, results in fierce competition.

Deposits still important to earnings trend

We have grown our deposit volumes significantly since 2022, when the Riksbank first hiked interest rates. Deposits grew almost 19% in 2024, an exceptional performance of which we are extremely proud. Deposits continue to comprise an important source of funding that supports our earnings performance and our ability to deliver competitive terms for mortgages and housing finance to our customers over time.

In early 2025, deposits experienced a slight trend break, mainly driven by increased outflows of fixed-term retail deposits. However, in the latter part of the quarter, we noted a stronger performance. For the quarter as a whole, deposits decreased marginally with 0.3% to SEK 255.0 billion. We continue to offer our customers good interest rates and fair conditions, not least when compared with the major banks, which are once again nearing zero interest on many account types. We are also investing considerable time and resources in improving and raising the visibility of our offer with the ambition of further growing our market shares.

New regulations improve our capital position

At the turn of the year, the new Banking Package (Capital Requirements Regulations III (CRR III)) entered force. The main impact of the new rules for SBAB entails that the risk weights for some of our corporate exposures are significantly reduced, a change which we welcome since it better reflects the low risk nature of our lending. All other factors remaining equal, the new rules mean we need to hold less capital and increase the scope measured against our risk-weighted capital requirements from the Swedish FSA.

We are governed by the goals that apply to our operations. We have a capital target set by our owner, the Swedish state, which entails maintaining a CET1 capital ratio and a total capital ratio of not less than 0.6 percentage points above the Swedish FSA’s communicated requirements. As CEO with operational responsibility for the business, I have also previously decided a supplementary capital target for CET1 capital, which entails SBAB maintaining a buffer equivalent to 1–3 percentage points above the Swedish FSA’s communicated requirements over time. At the end of the first quarter, our CET1 capital ratio was 14.4%, compared with the Swedish FSA’s requirement of 10.1%.

Stable financial performance and good resilience to market turbulence and volatility

Continued pressure on mortgage margins contributes to certain challenges in terms of maintaining operational profitability. Return on equity for the first quarter amounted to 10.1%. To a limited extent, raising the share of financing from deposits helps compensate for the low mortgage margins. Our underlying trend for net interest income remains stable, although net interest income dipped marginally quarter-on-quarter, as a result of some positive effects in the comparative period in terms of the reversal of the national deposit guarantee fee, which was slightly lower than our forecast for 2024.

The current situation is complex with an escalating trade war, mainly between the USA and China, causing sharp movements in financial markets and increased uncertainty about future developments. The long-term effects are difficult to assess. However, SBAB has a strong position and our capacity and preparedness to manage further disruptions is robust. At the end of the first quarter, we had raised slightly more than half of our estimated borrowing requirement for the full year and the credit quality in our lending portfolio remains very strong.

Wishing you a wonderful spring.

Mikael Inglander

CEO of SBAB

For further information, please contact:

Catharina Henriksson, Head of Press, SBAB

Telephone: +46 76-118 79 14

E-mail: catharina.henriksson@sbab.se

.