SBAB Year-end Report 2023

SBAB’s Year-end Report 2023 is now available for download on sbab.se/IR.

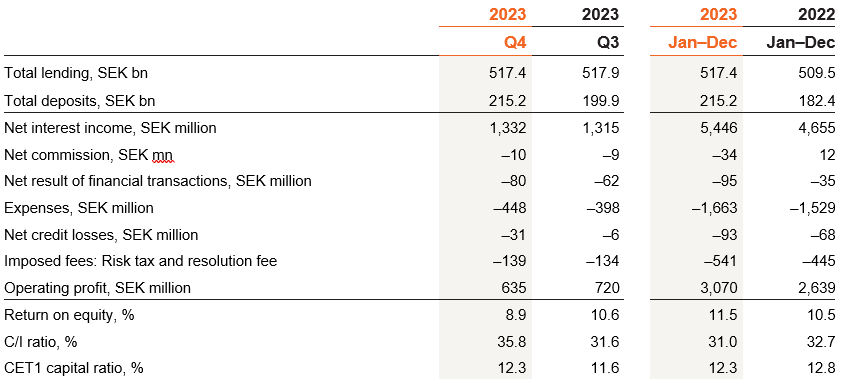

Q4 2023 (Q3 2023)

• Total lending decreased 0.1% to SEK 517.4 billion (517.9) for the quarter. Total deposits increased 7.7% to SEK 215.2 billion (199.9).

• Operating profit decreased 11.8% to SEK 635 million (720), primarily due to a more negative outcome for net income from financial transactions, increased costs and higher credit losses.

• Net interest income increased to SEK 1,332 million (1,315), mainly due to somewhat higher mortgage lending margins. This trend was partly offset by increased fees for national deposit guarantees and by somewhat lower deposit margins.

• Net credit losses increased to SEK 31 million (6), primarily due to adjustments in the impairment model and subsequent increases in credit loss allowances. Confirmed credit losses totalled SEK 2 million (2).

• The return on equity amounted to 8.9% (10.6) and the C/I ratio was 35.8% (31.6).

• The Common Equity Tier 1 (CET1) capital ratio was 12.3% (11.6).

• According to Swedish Quality Index (Svenskt Kvalitetsindex, SKI), SBAB had the most satisfied customers in Sweden in terms of residential mortgages to private individuals and property loans to corporates and tenant-owners’ associations for the fifth and sixth consecutive years, respectively.

January–December 2023 (January–December 2022)

• Total lending increased 1.6% during the year to SEK 517.4 billion (509.5) Total deposits increased 18.0% to SEK 215.2 billion (182.4).

• Operating profit grew 17.0% to SEK 3,070 million (2,639), primarily due to strong net interest income trend.

• Net interest income rose to SEK 5,446 million (4,655), primarily due to an increased share of financing from deposits and continued healthy deposit margins. Decreased lending margins for mortgages had a negative impact on the item.

• Net credit losses totalled SEK 93 million (68), the majority of which consisted of credit loss allowances. Confirmed credit losses totalled SEK 9 million (7).

• Imposed fees for the full year 2023 totalled SEK 541 million (445), of which the risk tax amounted to SEK 359 million (261) and the resolution fee to SEK 182 million (184).

• The return on equity amounted to 11.5% (10.5) and the C/I ratio was 31.0% (32.7).

• The Common Equity Tier 1 (CET1) capital ratio was 12.3% (12.8).

• The basis for the Board regarding appropriation of profits for 2023 is to propose a dividend of SEK 963 million, representing 40% of the Group’s net profit for the year after tax, in accordance with SBAB’s dividend policy.

Financial information

CEO statement from Mikael Inglander

Despite a challenging operating environment, we are once again putting a successful year behind us. We continue to attract new customers and grow our business volumes, not least within deposits, and we continue to have the highest levels of customer satisfaction in the industry. Our responsible approach to conducting our operations, together with our ability to adapt to changing conditions, comprise key factors behind this solid performance.

First and foremost – it was a tough year for many households and companies. War and other tumultuous events led to significant uncertainty and made the future both difficult to predict and tricky to navigate. During the last two years, inflation has climbed to levels not seen in several decades, leading to a series of policy rate hikes from the Riksbank. The pace and scope of the recent rate hikes were likely a surprise to many, and measures from the Riksbank had wide-ranging effects on the economy and society. Rising interest rates and increasing costs have eroded purchasing power and squeezed financial margins.

Even if some amount of uncertainty prevails regarding future economic trends, the resilience of the majority of households and businesses, and their ability to adapt, appear to be healthy. Despite market developments, at SBAB we have not noted any significant overall changes in the credit quality of our lending portfolio. This is proof that we run a stable, responsible business and that the assets in our balance sheet are of high quality. Credit losses totalled SEK 93 million for the full year, the majority of which consisted of credit loss allowances. Confirmed credit losses totalled SEK 9 million.

Sights set on interest rate cuts in 2024

The most recent economic trends and falling inflation point to interest rate cuts in 2024. We believe that the Riksbank will start to lower the interest rate starting from the summer. This means, all else being equal, that conditions for our customers will improve. It is also a positive sign that many property companies are continuing to act in order to adapt their operations and debt structure to a new interest rate environment. This includes lowering or postponing dividends, conducting new issues and selling assets.

High interest rates are expected to hold back demand for housing in 2024. Since their peak in spring 2022, housing prices have dipped around 16%, according to statistics from Booli. Prices for apartments have dropped nearly 12% and house prices approximately 18%. The decrease for the full-year 2023 hovered around a moderate 0.8%, primarily because of a relatively strong performance during the first half of the year.

Sweden’s most satisfied customers

Even if the business environment appears somewhat more challenging, at SBAB we continue to focus on being a growth-oriented and responsible player in the market. We continue to grow and we are proud that so many customers are turning to us to finance their homes or to manage and get a return on their savings. I am pleased and grateful that we have Sweden’s most satisfied residential mortgage customers according to Swedish Quality Index (Svenskt Kvalitetsindex, SKI) for the fifth consecutive year. According to the same survey, we also have Sweden’s most satisfied customers within property loans to tenant-owners’ associations and property companies. Fantastic!

Our lending grew 1.6% to a total of SEK 517.4 billion during the year. This is significantly lower growth than previous years, primarily due to the weaker housing market. Annual market growth for mortgages in November 2023 amounted to 0.7%, compared with 4.0% one year ago. We will likely continue to see relatively low market growth in 2024 before activity in the housing market recovers. Demand from property companies for bank financing has increased in pace with growing limitations in access to the bond market, which is expected to maintain credit growth in this segment.

Market transparency moving in the wrong direction

Our ambition is to offer our customers simple and competitive terms. This is how we help create a better, more functional market. Offering simple and competitive terms is also important for our ability to grow operations through attracting new customers and to retain our high level of customer satisfaction.

Our strategy for pricing involves ensuring a balance between mortgage rates and borrowing costs. Simply put – being transparent. This also applies to our terms for our savings accounts. The difference between listed rates and what customers ultimately pay for their mortgages, actual mortgage interest rates, increased for the industry as a whole in 2023. This is an unfortunate development which means that customers that are not actively negotiating their terms risk paying far too much for their mortgages. You can see the same pattern in the market for deposits: many players, not least the major, more established banks, continue to offer their customers far too little in terms of interest on savings. This is where we want to challenge and make a difference.

Long-term market interest rates have fallen sharply recently. This, in turn, means a decrease in SBAB’s borrowing costs. That is why during the quarter we chose, on several occasions, to lower our mortgage rates for longer maturities. Likewise, during the year we adjusted interest rates upwards for our savings accounts in pace with the policy rate hikes from the Riksbank.

A strong full-year performance and exceptional growth in deposits

We posted a strong financial performance and continued good profitability for the full year. Return on equity in 2023 amounted to 11.5%. Our net interest income continues to post a healthy trend. Net interest income increased 17.0% to SEK 5,446 million in 2023, despite very low residential mortgage margins. As borrowing costs rose through mortgage bonds, deposits have come to play an increasingly important role as a source of funding for our financial performance as well as our ability to offer competitive terms to our customers. As previously announced during the year, we continued to invest a great deal of time and resources to refine and develop our savings offering. During the fourth quarter we launched a fixed-interest account for retail customers, which was immediately successfully and highly appreciated by our customers. Deposits grew a full SEK 33 billion during the year, corresponding to 18.0%. This was an excellent performance that we are extremely proud of. That so many customers are choosing to save money with SBAB highlights the appeal of our offering and the strength of our brand. It is also a signal to other players in the market that many customers will no longer accept inferior terms.

Our service model, where the majority of customers meet us digitally or over the phone, allows for relatively efficient operations. At the same time, banking operations are becoming increasingly complex and demanding. This is due in part to increased digitalisation and changing customer needs but also in part to regulatory developments. We continued to invest in operations and costs increased 8.8% during the year to a total of SEK 1,663 million. The C/I ratio was 31.0%.

In 2021, SBAB decided to acquire Boappa in order to supplement and expand our existing offering of services within housing and household finances for tenant-owners’ associations. The company’s services are no doubt appreciated by its users, but the company has not grown or developed at the rate we had hoped for. Nor have we managed to integrate Boappa as a value-generating part of our customer offering and as a natural part of SBAB’s business. Our assessment is that it would require significant investment and resources from SBAB to turn this trend around. That is why we divested the company during the fourth quarter. We will continue to develop value-generating services to help our customers within the framework of our existing brands.

Now we look forward to an exciting 2024

I would like to take this opportunity to extend my sincere appreciation to all of our employees at SBAB for your dedication and efforts in 2023. I’m proud to lead an organisation with such skilled, driven and considerate individuals. Together, we make a difference.

Now we look forward to an exciting and eventful 2024.

Mikael Inglander

CEO of SBAB

For more information, please contact:

Catharina Henriksson, Head of Press SBAB

Telephone: +46 76-118 79 14

E-mail: catharina.henriksson@sbab.se