SBAB Interim Report Jan–Sep 2023

SBAB’s Interim Report January-September 2023 is now available for download on sbab.se/IR.

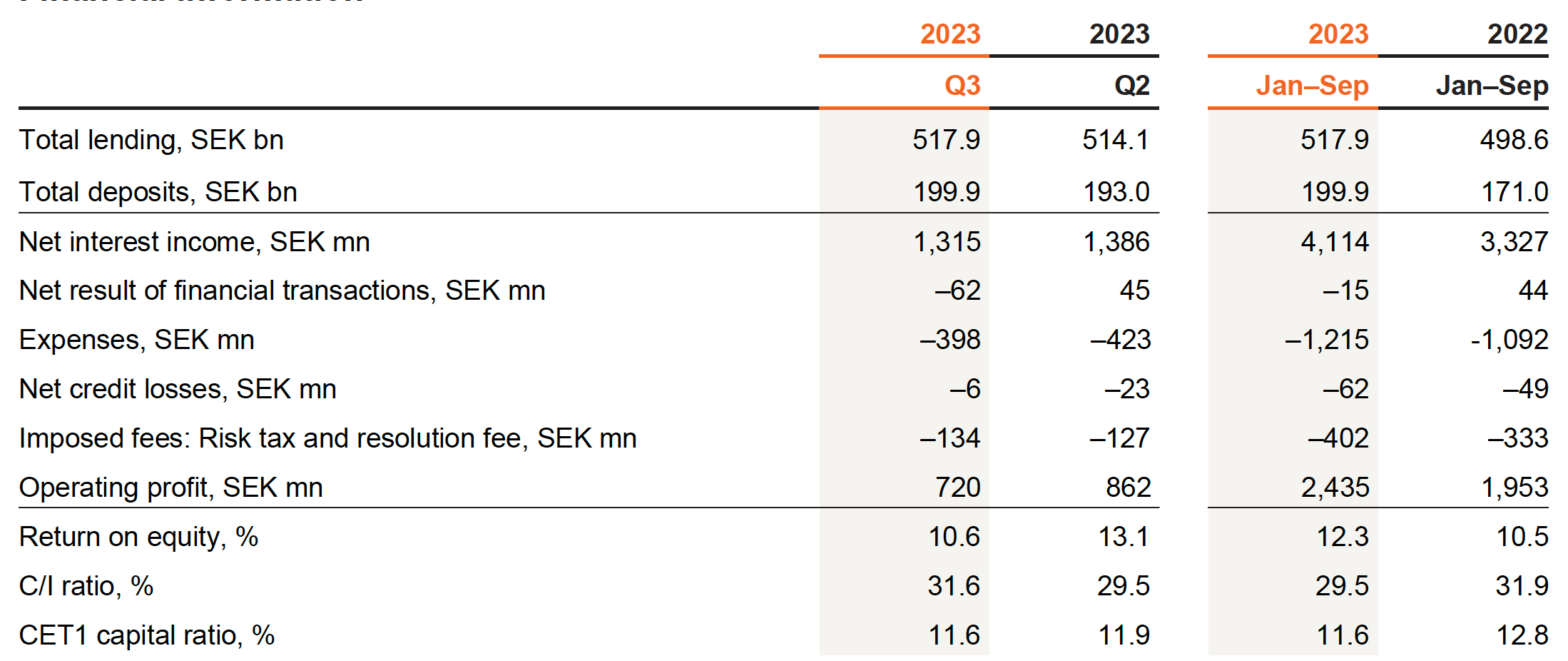

Q3 2023 (Q2 2023)

- Total lending increased 0.7% to SEK 517.9 billion (514.1) for the quarter.

- Total deposits increased 3.6% to SEK 199.9 billion (193.0).

- Operating profit decreased 16.5% to SEK 720 million (862), primarily due to lower net interest income and a more negative outcome for the net result of financial transactions.

- Net interest income declined to SEK 1,315 million (1,386), mainly due to the continued contraction of mortgage lending margins. An increased share of financing from deposits positively impacted the item.

- Net credit losses amounted to SEK 6 million (23). Confirmed credit losses totalled SEK 2 million (3).

- Imposed fees totalled SEK 134 million (127) for the quarter, of which the risk tax amounted to SEK 89 million (88) and the resolution fee to SEK 45 million (39).

- The return on equity amounted to 10.6% (13.1) and the C/I ratio was 31.6% (29.5).

- The Common Equity Tier 1 (CET1) capital ratio was 11.6% (11.9).

Financial information

CEO statement from Mikael Inglander

We launched our first savings account just over 15 years ago. Today we have over half a million savings customers and are approaching a deposit volume that exceeds SEK 200 billion. This is a very welcome development that we are incredibly proud of.

As expected, the Riksbank decided to raise the policy rate an additional 0.25 percentage points to a total of 4.00% at its most recent meeting in September, based on persistently high inflation, not least within the service sector, and a weak krona. It also signalled that the policy rate could be raised further and that we shouldn’t expect any decreases in the near future.

We think it’s possible that inflation is decreasing somewhat faster than what the Riksbank is suggesting. In our view, the Riksbank places too much weight on inflation trends in the last year instead of taking inflation’s recent short-term performance into consideration. It is also important to review expectations for future inflation trends. It takes a relatively long time for a higher policy rate to affect households and companies, and thereby to affect price trends. The policy rate hikes that have been carried out to date have likely not had their full effect on the economy or inflation. It is unfortunately difficult to assess inflation and considerable uncertainty regarding future developments still prevails. However, a reasonable assessment is nonetheless that the policy rate, and therefore also mortgage interest rates, are now approaching their peak.

We are capturing market shares in a slowing market

Activity in the housing market remains low. In the last three months, the number of homes sold was 23% lower than in the year-earlier period. High interest rates in combination with falling housing prices in the secondary market have put pressure on housing construction, which is why the rate of new production has decreased drastically in such a short time.

Prices for apartments and houses fell substantially in 2022, especially for houses. So far this year, the price trend has been positive for apartments as well as houses. However, we believe that housing prices will decrease further in the near term. This means that we expect the total price decline, calculated from a peak in early 2022, will amount to around 20%. As of 2024, housing prices are expected to once again increase, which means that there appears to be some change of direction in this area as well.

Credit growth in the residential mortgage market remains very low. Annualised growth in August was around 1%, compared to close to 6% at the same time the previous year. Market growth was even negative in some months of 2023. Competition in the market is tough and the margins remain under pressure.

Our long-term ambition is to grow lending. Even if the current market conditions are challenging, we are continuing to gain ground and capture market shares. Important success factors in the current market include simplicity, consideration and transparency: factors that have long been important parts of SBAB’s corporate culture and offering. Total lending increased nearly 1% during the third quarter to SEK 517.9 billion.

SBAB’s deposit volume approaching SEK 200 billion!

SBAB launched savings accounts for private individuals as recently as 2007. Two years later, in 2009, we complemented our offering to include savings for companies and organisations. Now, just over 15 years later, we are close to reaching a deposit volume in excess of SEK 200 billion. Naturally, we are pleased and proud that so many customers are choosing to save and earn interest with us.

As interest rate hikes came from the Riksbank, we continuously adjusted the interest rate on our savings accounts upwards. It feels good to be able to share a beneficial offering with our customers. It is also clear that many customers see SBAB as a more attractive alternative than many other players in the market.

I have previously highlighted how important it is for SBAB to achieve a more diversified funding mix, in part to reduce volatility in our earnings over time but also to reduce our relative dependence on capital market funding. Right now we are investing a lot of time and resources in further refining our savings offering, in terms of product offering and terms as well as in terms of user friendliness and simplicity. We are also investing resources in making SBAB visible in the market, including in certain growth regions where we have not traditionally been as strong.

SBAB’s good credit quality confirmed in stress test from the EBA

SBAB’s overall credit quality remains good. Our operations are primarily built on issuing loans against collateral. This means that our lending portfolio is characterised by low risk and that we have the ability to manage weaker market conditions. This was confirmed by the European Banking Authority (EBA) and its comprehensive EU-wide stress test that investigated the resiliency of financial institutions when it comes to dramatic disruptions in the operating environment and economy. SBAB had some of the strongest results of all the banks included in the test.

Credit losses for January to September 2023 amounted to SEK 62 million, which corresponds to a credit loss ratio of 0.02% and primarily consisted of loss allowances for future credit losses. Actual credit losses remained low and totalled SEK 7 million for the period. The share of credit stage 3 loans – meaning loans that are deemed to be especially high-risk – increased somewhat at the aggregate level during the year, albeit from very low levels. This share amounted to 0.11% of our total lending at the end of the third quarter. We are not ruling out additional impacts on credit quality later in the credit cycle, when interest rate hikes have been fully absorbed by households, companies and the economy.

Stable financial performance

Our net interest income continues to post a stable trend despite historically low residential mortgage margins. This is where deposits play an important role. Generally, increases in mortgage rates have not been in line with those for the Riksbank’s policy rate nor with the banks’ borrowing costs via mortgage bonds. One of the underlying reasons is that many banks have instead kept interest rates low on their savings accounts. In this matter, I think that keeping pace with the Riksbank’s interest rate hikes is, and has been, lacking in large parts of the industry. For us at SBAB, it is very important to continuously adjust our interest rates for lending as well as deposits to reflect the prevailing market conditions. Net interest income for the quarter amounted to SEK 1,315 million, up 14% year-on-year. Compared with the previous quarter, net interest income declined 5%. Return on equity for the quarter was 10.6%, which exceeds the return target of 10% set by our owner, the Swedish government.

Activities aimed at reaching the climate goal

Much is happening within sustainability. New insights and regulatory requirements from authorities are accelerating developments. Late last year, SBAB decided on a new long-term climate goal that lasts until 2038. We know that it will require a lot of initiatives and hard work to reach the goal, but we are determined to succeed.

It has become clear that many of our customers – property companies not least among them – are facing challenges similar to ours. We need to be able to provide relevant products and services to help and support our customers in their work. We recently disbursed our first sustainability-linked loan to a corporate customer. This is a loan that will be used to accomplish a transition within sustainability, for example improving the energy performance of a property. Any such transition needs to be comprehensive in scope, and require extra investment on account of the challenge it presents. This means our goal is to be able to say that the money enabled a transition that would not otherwise have happened. To do this, we set several targets that are followed up annually. The customer receives somewhat lower interest in exchange for a promise to deliver improvements. Conversely, if the agreed-upon progress is not made, the customer needs to pay somewhat higher interest.

One activity out of many on the journey to reaching our long-term goal.

Have a wonderful autumn.

Mikael Inglander

CEO of SBAB

For more information, please contact:

Mikael Inglander, CEO SBAB

Telephone: +46 8-614 43 28

E-mail: mikael.inglander@sbab.se

Bessie Wedholm, Acting Head of Press SBAB

Telephone: +46 73-049 08 74

E-mail: bessie.wedholm@sbab.se